1. Personal Finance

|

In the realm of investments women's caution often leads to impressive returns. Here we will explore the need to reimagine personal finance with women at the center and for women to stay informed and advocate for policies that not only fortify retirement programs but champion gender equity. Buckle up for a journey through the intricacies of personal finance with a keen focus on empowering women for a financially resilient future.

|

Personal Finance

Numerous studies have shown that there are gendered differences in the way parents raise girls and boys. Some of those differences even begin as far back as in the womb. When it comes to economics, girls and boys are raised to handle money differently, and this has profound effects on their financial futures. In sum, girls are raised to protect money and save it, while boys are raised to go after money and invest in it.

The symbols of wealth Also send subtle messages to girls. The symbol of Wall Street is a huge statue of a bull, snorting and grunting at passers by. Only recently was the statue of a small girl, staring him down, added. State money also emphasizes the maleness of money. With no permanent exception, every American bill features a male figure from history: a past president.

And if that wasn’t enough, only 26% of people who work in finance are female, so most advice is tailored to the male experience. Women’s financial futures are actually distinctly different from males. 74% of women die single, because most women outlive their male partners, therefore, retirement planning is crucial. Women also have to financially plan for the birth of their first child, which, after study shows, has a massive financial impact on women, known as the motherhood penalty. More on that in microeconomics.

So given that women are going to lose money, when they have their first child, and given that they are going to likely die, single women must pragmatically take control of their financial futures, and safe investing and saving is insufficient.

Numerous studies have shown that there are gendered differences in the way parents raise girls and boys. Some of those differences even begin as far back as in the womb. When it comes to economics, girls and boys are raised to handle money differently, and this has profound effects on their financial futures. In sum, girls are raised to protect money and save it, while boys are raised to go after money and invest in it.

The symbols of wealth Also send subtle messages to girls. The symbol of Wall Street is a huge statue of a bull, snorting and grunting at passers by. Only recently was the statue of a small girl, staring him down, added. State money also emphasizes the maleness of money. With no permanent exception, every American bill features a male figure from history: a past president.

And if that wasn’t enough, only 26% of people who work in finance are female, so most advice is tailored to the male experience. Women’s financial futures are actually distinctly different from males. 74% of women die single, because most women outlive their male partners, therefore, retirement planning is crucial. Women also have to financially plan for the birth of their first child, which, after study shows, has a massive financial impact on women, known as the motherhood penalty. More on that in microeconomics.

So given that women are going to lose money, when they have their first child, and given that they are going to likely die, single women must pragmatically take control of their financial futures, and safe investing and saving is insufficient.

Selecting the “Right” Career

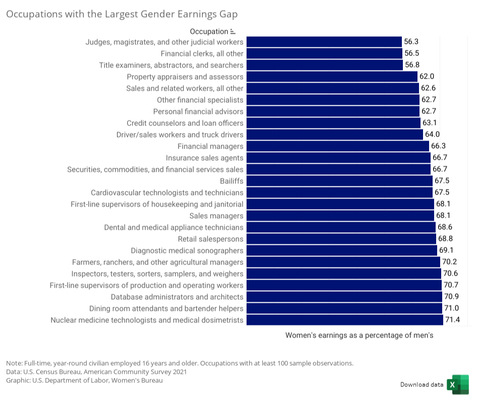

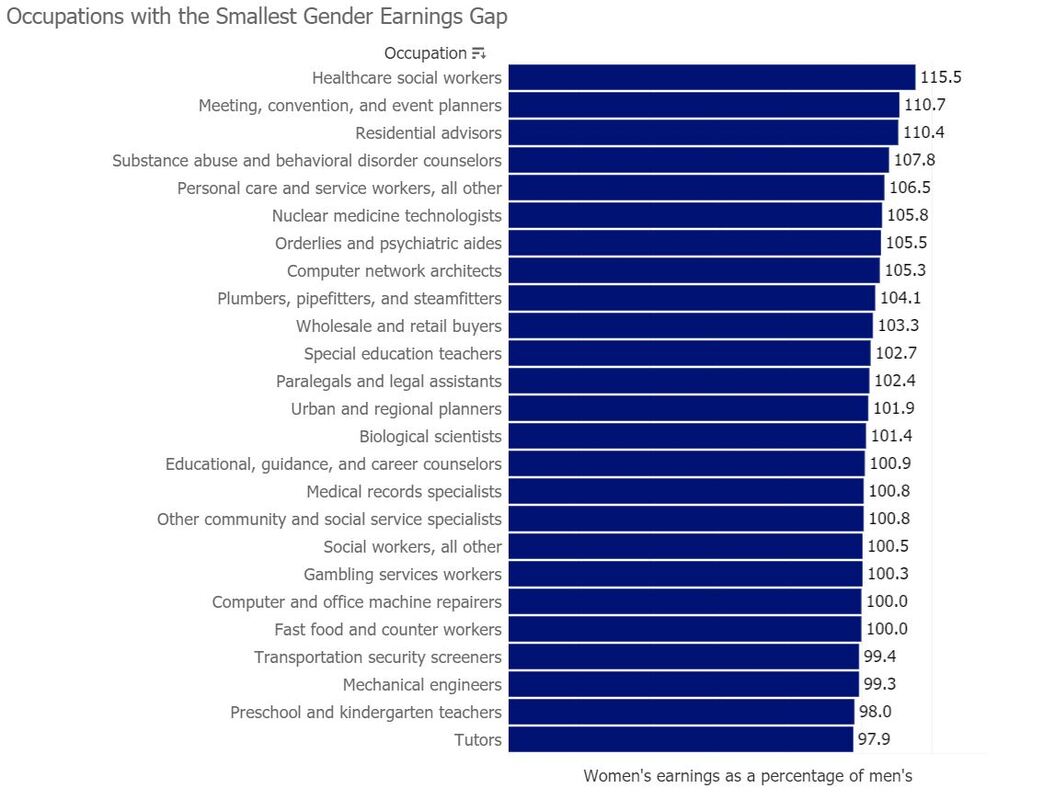

Most kids assume they will make more over the course of their life and career, the problem is that pay gaps that start in the first jobs can follow throughout a career. Studies show that the gender pay gap follows women throughout the workforce and into retirement. In some places, employers will ask prospective candidates about their salaries from prior jobs to determine how much to pay them at their new job, rather than offering them the maximum of what the job pays. The effect is a type of discrimination that follows women from job to job over the course of their life and effects them even into retirement due to less earned income and fewer Social Security and pension benefits.

A tried, and true strategy for women is to find career fields that offer flexibility around child rearing. Teaching positions generally provide a stable and consistent salary, offering financial security for mothers. Unlike some professions with irregular income patterns or commission-based structures, teachers can rely on a regular paycheck. This stability is particularly crucial for mothers who are often juggling various expenses associated with raising a family. The alignment of a teacher's schedule with that of their children is a distinct advantage. Teachers usually follow a school calendar, which includes breaks and vacations that coincide with those of their children. This synchronization allows mothers to spend quality time with their kids during holidays and enjoy a more harmonious work-life balance.

Teachers often benefit from parental leave options due to the influence of teachers unions. These unions advocate for family-friendly policies, including maternity and paternity leave, allowing mothers to take time off to care for their newborns without sacrificing job security or financial stability. This support is invaluable during the crucial early stages of a child's life. That said, those jobs are notoriously underpaid, because they have a history of being done by women and sexism, has long impacted how women were paid in the workforce. Women’s income through most of history was seen as secondary or supplementary to the male head of household income.

While teaching offers unique advantages, other professions within the education sector, such as administrative roles, and even health-related careers, can also provide similar benefits. Administrators in educational institutions and healthcare professionals may enjoy stable salaries and certain family-friendly policies. However, they might not align as closely with school calendars, missing the advantage of synchronized schedules with children.

But, as Gloria Stinem said, children have two parents, and the full pressure of having a flexible job for child rearing doesn’t have to fall on the mother. In recent decades, significant strides have been made in breaking down gender stereotypes and regulations protecting female employees and mothers, particularly in traditionally male-dominated fields like science, medicine, engineering, law, and the military. The representation of women in law schools, for instance, has increased substantially, with as many women as men enrolled by 2020. Similarly, the STEM field has seen progress, with women now constituting 27% of jobs, up from 13% in 1980. Despite challenges in the tech world, Claudia Goldin notes a decline in gender biases in most male-dominated professions.

Unlike the gender desegregation seen in male-dominated professions, the shift has been predominantly one-way, where women are increasingly taking on roles traditionally held by men. However, this positive trend has not extended to traditionally female occupations, particularly in the HEAL fields (health, education, administration, and literacy). These roles have become even more "pink collar," with just 26% of HEAL jobs held by men, down from 35% in 1980.

HEAL occupations, contrasting with STEM, emphasize people-centric tasks and prioritize literacy over numeracy skills. The decline in the male share is notable in certain fields, such as psychology and social work. For instance, the proportion of men in psychology has dropped from 39% to 29% in the last decade, with a mere 5% among psychologists aged 30 or younger. In teaching professions, the decline in male representation is evident, with only 24% of K-12 teachers being men, down from 33% in the early 1980s. The situation is more acute in early education, where men are virtually invisible, constituting only 3% of pre-K and kindergarten teachers, highlighting a concerning gender imbalance.

Increasingly women are looking at higher paid roles. In 2023 women surpassed men in law school. Nearly 40 percent of practicing lawyers are now women, marking a notable increase from the 31 percent recorded in 2010. The presence of female federal judges has also seen a substantial rise since 1980 when there were only 46; presently, approximately one-third of all federal judges are women, and this figure is on an upward trajectory. State Supreme Courts exhibit a robust representation of women, constituting 41 percent of high-court justices.

Women's leadership in U.S. law schools has witnessed a remarkable surge. In 2000, a mere 10 percent of law school deans were women, whereas today, 43 percent of all law school deans are women, as per Rosenblatt’s Deans Database. Additionally, women now make up 42.8 percent of law school faculty members, a significant jump from the 20 percent recorded in the 1980s. Despite these advancements, a notable gap persists in leadership positions, especially for women of color. Within law firms, women account for only 26.65 percent of partners and a mere 22.6 percent of equity partners, according to the National Association of Women Lawyers' recent diversity report on U.S. law firms. Another noteworthy trend is the substantial decline in male enrollment in law schools as women increasingly dominate classrooms. Over the past 13 years, the number of male enrollees has consistently decreased, dropping from 78,516 in 2010 to 50,097 in 2023.

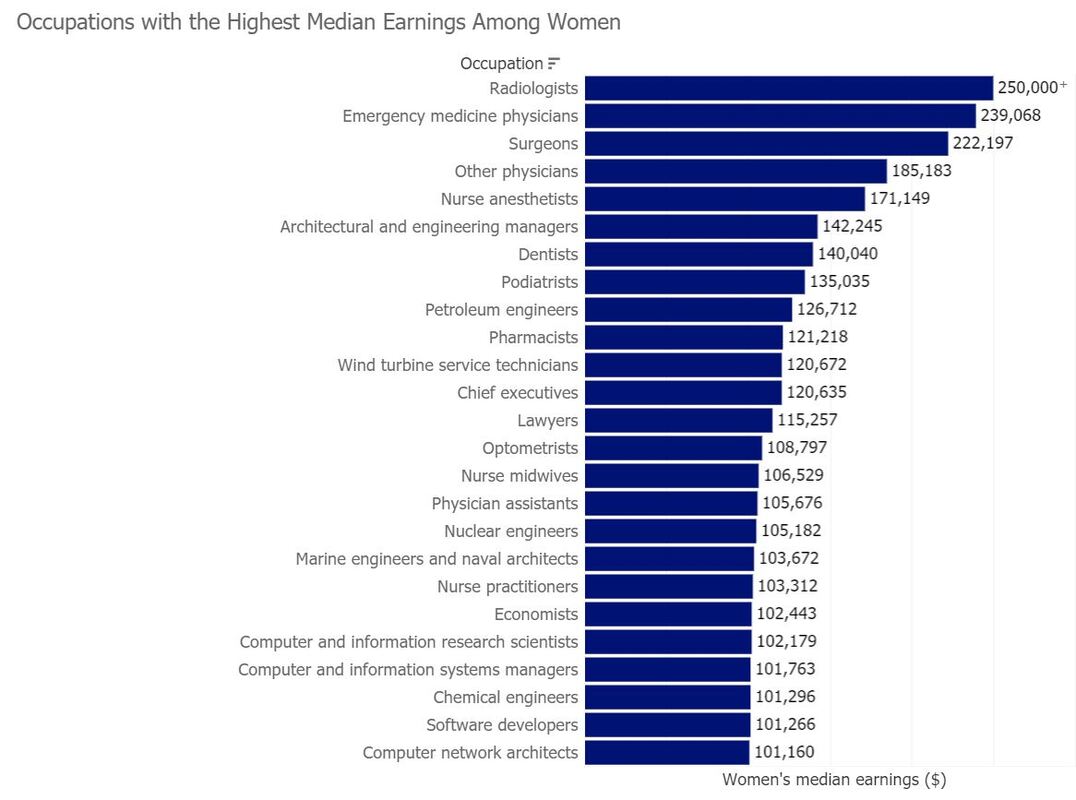

The legal profession is notoriously inflexible for parents and rewards people who build long-term relationships with clients. Clients want to know their lawyer personally, regardless of how skilled that person is. For some reason, the legal profession hasn’t shifted into the 21st-century to allow skilled lawyers to put in less time. For MBA and JD earners, there is a substantial gender earnings gap that increases over time. Notably, women with MBAs and JDs tend to shift into lower-paying positions or leave the workforce for temporal flexibility, especially after having children. The finance and corporate sectors penalize lower hours, leading to a pronounced gender earnings gap.

By contrast, Nobel Prize winning economist, Claudia Goldin’s research, showed that pharmacist earn comparable hourly income to lawyers, in fact, it’s one of the top paying jobs for women, but it has allowed parents, mostly women, to be more flexible on the job. When a customer shows up to a pharmacy, they don’t really care who’s preparing the medication for them. This adaptation of the field has highly skilled women to have lucrative careers as pharmacists. Goldin used the O*NET database to identify characteristics related to flexibility in various occupations and found a negative association between these characteristics and the corrected ratio of female to male earnings.

So what’s the take away? Young people should be thinking about the jobs that will allow them to have the lifestyle they want. If that lifestyle includes children, they need to be thinking about that and build it into their career planning.

Most kids assume they will make more over the course of their life and career, the problem is that pay gaps that start in the first jobs can follow throughout a career. Studies show that the gender pay gap follows women throughout the workforce and into retirement. In some places, employers will ask prospective candidates about their salaries from prior jobs to determine how much to pay them at their new job, rather than offering them the maximum of what the job pays. The effect is a type of discrimination that follows women from job to job over the course of their life and effects them even into retirement due to less earned income and fewer Social Security and pension benefits.

A tried, and true strategy for women is to find career fields that offer flexibility around child rearing. Teaching positions generally provide a stable and consistent salary, offering financial security for mothers. Unlike some professions with irregular income patterns or commission-based structures, teachers can rely on a regular paycheck. This stability is particularly crucial for mothers who are often juggling various expenses associated with raising a family. The alignment of a teacher's schedule with that of their children is a distinct advantage. Teachers usually follow a school calendar, which includes breaks and vacations that coincide with those of their children. This synchronization allows mothers to spend quality time with their kids during holidays and enjoy a more harmonious work-life balance.

Teachers often benefit from parental leave options due to the influence of teachers unions. These unions advocate for family-friendly policies, including maternity and paternity leave, allowing mothers to take time off to care for their newborns without sacrificing job security or financial stability. This support is invaluable during the crucial early stages of a child's life. That said, those jobs are notoriously underpaid, because they have a history of being done by women and sexism, has long impacted how women were paid in the workforce. Women’s income through most of history was seen as secondary or supplementary to the male head of household income.

While teaching offers unique advantages, other professions within the education sector, such as administrative roles, and even health-related careers, can also provide similar benefits. Administrators in educational institutions and healthcare professionals may enjoy stable salaries and certain family-friendly policies. However, they might not align as closely with school calendars, missing the advantage of synchronized schedules with children.

But, as Gloria Stinem said, children have two parents, and the full pressure of having a flexible job for child rearing doesn’t have to fall on the mother. In recent decades, significant strides have been made in breaking down gender stereotypes and regulations protecting female employees and mothers, particularly in traditionally male-dominated fields like science, medicine, engineering, law, and the military. The representation of women in law schools, for instance, has increased substantially, with as many women as men enrolled by 2020. Similarly, the STEM field has seen progress, with women now constituting 27% of jobs, up from 13% in 1980. Despite challenges in the tech world, Claudia Goldin notes a decline in gender biases in most male-dominated professions.

Unlike the gender desegregation seen in male-dominated professions, the shift has been predominantly one-way, where women are increasingly taking on roles traditionally held by men. However, this positive trend has not extended to traditionally female occupations, particularly in the HEAL fields (health, education, administration, and literacy). These roles have become even more "pink collar," with just 26% of HEAL jobs held by men, down from 35% in 1980.

HEAL occupations, contrasting with STEM, emphasize people-centric tasks and prioritize literacy over numeracy skills. The decline in the male share is notable in certain fields, such as psychology and social work. For instance, the proportion of men in psychology has dropped from 39% to 29% in the last decade, with a mere 5% among psychologists aged 30 or younger. In teaching professions, the decline in male representation is evident, with only 24% of K-12 teachers being men, down from 33% in the early 1980s. The situation is more acute in early education, where men are virtually invisible, constituting only 3% of pre-K and kindergarten teachers, highlighting a concerning gender imbalance.

Increasingly women are looking at higher paid roles. In 2023 women surpassed men in law school. Nearly 40 percent of practicing lawyers are now women, marking a notable increase from the 31 percent recorded in 2010. The presence of female federal judges has also seen a substantial rise since 1980 when there were only 46; presently, approximately one-third of all federal judges are women, and this figure is on an upward trajectory. State Supreme Courts exhibit a robust representation of women, constituting 41 percent of high-court justices.

Women's leadership in U.S. law schools has witnessed a remarkable surge. In 2000, a mere 10 percent of law school deans were women, whereas today, 43 percent of all law school deans are women, as per Rosenblatt’s Deans Database. Additionally, women now make up 42.8 percent of law school faculty members, a significant jump from the 20 percent recorded in the 1980s. Despite these advancements, a notable gap persists in leadership positions, especially for women of color. Within law firms, women account for only 26.65 percent of partners and a mere 22.6 percent of equity partners, according to the National Association of Women Lawyers' recent diversity report on U.S. law firms. Another noteworthy trend is the substantial decline in male enrollment in law schools as women increasingly dominate classrooms. Over the past 13 years, the number of male enrollees has consistently decreased, dropping from 78,516 in 2010 to 50,097 in 2023.

The legal profession is notoriously inflexible for parents and rewards people who build long-term relationships with clients. Clients want to know their lawyer personally, regardless of how skilled that person is. For some reason, the legal profession hasn’t shifted into the 21st-century to allow skilled lawyers to put in less time. For MBA and JD earners, there is a substantial gender earnings gap that increases over time. Notably, women with MBAs and JDs tend to shift into lower-paying positions or leave the workforce for temporal flexibility, especially after having children. The finance and corporate sectors penalize lower hours, leading to a pronounced gender earnings gap.

By contrast, Nobel Prize winning economist, Claudia Goldin’s research, showed that pharmacist earn comparable hourly income to lawyers, in fact, it’s one of the top paying jobs for women, but it has allowed parents, mostly women, to be more flexible on the job. When a customer shows up to a pharmacy, they don’t really care who’s preparing the medication for them. This adaptation of the field has highly skilled women to have lucrative careers as pharmacists. Goldin used the O*NET database to identify characteristics related to flexibility in various occupations and found a negative association between these characteristics and the corrected ratio of female to male earnings.

So what’s the take away? Young people should be thinking about the jobs that will allow them to have the lifestyle they want. If that lifestyle includes children, they need to be thinking about that and build it into their career planning.

US Department of Labor

|

US Department of Labor

|

Woman Making Investments, Stock Photo

Woman Making Investments, Stock Photo

Investing

Women need to embrace managing and dealing with money. According to polls, money is women’s number one stressor and that saving and investing helps women feel empowered and in control of their finances. Financial wellness is just as important as physical and mental wellness.

The gender wealth gap is the gap in overall wealth (not just pay) between men and women including assets, inheritance, and other aspects of wealth that can be generation. The wealth gap is larger than the pay gap– by a lot and is held in place by the historical and legal obstacles that have placed women, especially Black and Native American women, at a significant economic disadvantage. Even if the pay gap were eliminated, these systemic barriers would persist, encompassing issues such as slavery, Jim Crow, land sovereignty denial, unequal educational access, redlining, and modern-day inequities. If women don’t have wealth, it makes it tricky to invest it.

Still, studies show that women are more cautious investors. Taking lower levels of risk compared to their male counterparts. According to Wells Fargo, women typically assume around 82% of the investment risk taken by men and this isn’t necessarily a bad thing, as women tend to be better investors and are less inclined to hop on investment trends. This pays off, women investors achieve superior returns compared to their male counterparts, variances ranging from 0.4% to almost 1%. One encouraging discovery is the increasing interest in investing among younger women. According to Fidelity, 71% of millennial women engage in non-retirement investing, surpassing the rates for Gen Xers (67%) and baby boomers (62%).

Interestingly, women are more likely to remain composed amid market instability– a crucial skill in investing. According to Nationwide, only 8% of women opted to cash out their retirement accounts in such circumstances, compared to 15% of men. Selling during turbulent market conditions is generally ill-advised as stock prices tend to decline, potentially resulting in financial losses. It is more prudent to retain investments during downturns, allowing the portfolio to recover over time.

There are interesting threats to the wealth gap including the Great Wealth Transfer, an anticipated shift in who owns wealth happens. Currently, half of the nation's wealth belongs to the Baby Boomer generation. Over the next two decades, this wealth will be inherited, resulting in a transfer of wealth on an unprecedented scale. Estimates vary on the exact magnitude of this wealth transfer, but by 2030 American women are projected to oversee at least $30 trillion, constituting a historic transformation. When women control more wealth, they can invest it, and women have historically invested differently than men.

With women controlling more and more wealth, there will be a sea change in what gets funding as women tend to invest much differently than men. Philanthropy is one area where women, particularly those with high net worth, tend to excel. High-net-worth women typically contribute a substantial portion of their wealth to philanthropic causes. With more women gaining wealth during the Great Wealth Transfer, nonprofits may experience increased funding. Not surprisingly, female investors tend to show more support for organizations helping women and girls and addressing issues such as reproductive rights, women's health, and violence against women.

Other women may use their wealth to start businesses, contributing to economic growth. Companies led by women often outperform those without female leadership. This suggests a positive impact on entrepreneurship and economic development. Studies indicate that women are already more likely to engage in impact investing, including gender-lens investing, which evaluates companies based on their gender-related practices. Women also express a strong interest in climate-themed investments.

Despite outperforming men in investing, women exhibit lower confidence levels in this domain. Fidelity's findings reveal that only one-third of women perceive themselves as investors, and the majority lack confidence in making investment decisions. Data from FINRA reveals that this insecurity may be fueled by a clear knowledge gap with 64% of women respondents having low investing knowledge. Still, women’s successes suggest higher knowledge is not necessarily a prerequisite for successful investing– so women should leave their insecurity at the door.

Women need to embrace managing and dealing with money. According to polls, money is women’s number one stressor and that saving and investing helps women feel empowered and in control of their finances. Financial wellness is just as important as physical and mental wellness.

The gender wealth gap is the gap in overall wealth (not just pay) between men and women including assets, inheritance, and other aspects of wealth that can be generation. The wealth gap is larger than the pay gap– by a lot and is held in place by the historical and legal obstacles that have placed women, especially Black and Native American women, at a significant economic disadvantage. Even if the pay gap were eliminated, these systemic barriers would persist, encompassing issues such as slavery, Jim Crow, land sovereignty denial, unequal educational access, redlining, and modern-day inequities. If women don’t have wealth, it makes it tricky to invest it.

Still, studies show that women are more cautious investors. Taking lower levels of risk compared to their male counterparts. According to Wells Fargo, women typically assume around 82% of the investment risk taken by men and this isn’t necessarily a bad thing, as women tend to be better investors and are less inclined to hop on investment trends. This pays off, women investors achieve superior returns compared to their male counterparts, variances ranging from 0.4% to almost 1%. One encouraging discovery is the increasing interest in investing among younger women. According to Fidelity, 71% of millennial women engage in non-retirement investing, surpassing the rates for Gen Xers (67%) and baby boomers (62%).

Interestingly, women are more likely to remain composed amid market instability– a crucial skill in investing. According to Nationwide, only 8% of women opted to cash out their retirement accounts in such circumstances, compared to 15% of men. Selling during turbulent market conditions is generally ill-advised as stock prices tend to decline, potentially resulting in financial losses. It is more prudent to retain investments during downturns, allowing the portfolio to recover over time.

There are interesting threats to the wealth gap including the Great Wealth Transfer, an anticipated shift in who owns wealth happens. Currently, half of the nation's wealth belongs to the Baby Boomer generation. Over the next two decades, this wealth will be inherited, resulting in a transfer of wealth on an unprecedented scale. Estimates vary on the exact magnitude of this wealth transfer, but by 2030 American women are projected to oversee at least $30 trillion, constituting a historic transformation. When women control more wealth, they can invest it, and women have historically invested differently than men.

With women controlling more and more wealth, there will be a sea change in what gets funding as women tend to invest much differently than men. Philanthropy is one area where women, particularly those with high net worth, tend to excel. High-net-worth women typically contribute a substantial portion of their wealth to philanthropic causes. With more women gaining wealth during the Great Wealth Transfer, nonprofits may experience increased funding. Not surprisingly, female investors tend to show more support for organizations helping women and girls and addressing issues such as reproductive rights, women's health, and violence against women.

Other women may use their wealth to start businesses, contributing to economic growth. Companies led by women often outperform those without female leadership. This suggests a positive impact on entrepreneurship and economic development. Studies indicate that women are already more likely to engage in impact investing, including gender-lens investing, which evaluates companies based on their gender-related practices. Women also express a strong interest in climate-themed investments.

Despite outperforming men in investing, women exhibit lower confidence levels in this domain. Fidelity's findings reveal that only one-third of women perceive themselves as investors, and the majority lack confidence in making investment decisions. Data from FINRA reveals that this insecurity may be fueled by a clear knowledge gap with 64% of women respondents having low investing knowledge. Still, women’s successes suggest higher knowledge is not necessarily a prerequisite for successful investing– so women should leave their insecurity at the door.

Women Planning for Retirement, Stock Photo

Women Planning for Retirement, Stock Photo

Retirement Planning

Throughout their life, women experience an income disparity, with the most pronounced gap occurring in retirement. The gender pay gap, persisting throughout a woman's life, leads to substantial earnings losses, hindering savings accumulation. Women fall have smaller Social Security funds, pensions, and savings. Consequently, their retirement income is only 70% of that earned by men.

Elderly women are more prone to living below the poverty line compared to men. Notably, in 2018, 62% of Americans above 65 living in poverty were women. Women, often engaged in part-time work or navigating in and out of the workforce for caregiving, struggle to save for retirement and frequently lack access to employer-sponsored retirement plans. Lower wages and intermittent employment result in reduced Social Security benefits. The data show 11% of women above 65 lived in poverty, while just 8% of men. Even those not in poverty struggle with meager incomes. While white men aged over 65 average $44,200 annually, Black women have $21,900, Latinas $14,800, and white women $23,100– almost half the available funds!

Despite living longer, women face higher retirement costs, including daily living and healthcare expenses. Social Security is a crucial income source, constituting 47% of total income for unmarried women, including widows, compared to 34% for unmarried men. Additionally, 46% of unmarried women over 65 heavily rely on Social Security for almost all (90% or more) of their income.

Ensuring a secure retirement for American women, regardless of their career paths, necessitates laws and policies fortifying retirement programs. This involves safeguarding Social Security, enhancing pension benefits, and advocating for fair pay throughout women's careers. Achieving gender equity is an enduring commitment.

Conclusion

It is a pivotal moment to reimagine personal finance with women in mind. It is crucial to dismantle gender differences in financial upbringing and their impacts on women's financial futures.Women must take control of their financial futures, especially considering unique challenges like the motherhood penalty and the fact that 74% of women may end up single in retirement. Therefore, young women should carefully explore career choices considering the gender pay gap and the importance of selecting fields with flexibility around child-rearing. In terms of investing, women are found to be more cautious but achieve superior returns. With the looming Great Wealth Transfer women will have greater opportunities to influence investment patterns and philanthropy. Finally, it’s important to be aware of and advocate for policies that fortify retirement programs and promote gender equity.

Throughout their life, women experience an income disparity, with the most pronounced gap occurring in retirement. The gender pay gap, persisting throughout a woman's life, leads to substantial earnings losses, hindering savings accumulation. Women fall have smaller Social Security funds, pensions, and savings. Consequently, their retirement income is only 70% of that earned by men.

Elderly women are more prone to living below the poverty line compared to men. Notably, in 2018, 62% of Americans above 65 living in poverty were women. Women, often engaged in part-time work or navigating in and out of the workforce for caregiving, struggle to save for retirement and frequently lack access to employer-sponsored retirement plans. Lower wages and intermittent employment result in reduced Social Security benefits. The data show 11% of women above 65 lived in poverty, while just 8% of men. Even those not in poverty struggle with meager incomes. While white men aged over 65 average $44,200 annually, Black women have $21,900, Latinas $14,800, and white women $23,100– almost half the available funds!

Despite living longer, women face higher retirement costs, including daily living and healthcare expenses. Social Security is a crucial income source, constituting 47% of total income for unmarried women, including widows, compared to 34% for unmarried men. Additionally, 46% of unmarried women over 65 heavily rely on Social Security for almost all (90% or more) of their income.

Ensuring a secure retirement for American women, regardless of their career paths, necessitates laws and policies fortifying retirement programs. This involves safeguarding Social Security, enhancing pension benefits, and advocating for fair pay throughout women's careers. Achieving gender equity is an enduring commitment.

Conclusion

It is a pivotal moment to reimagine personal finance with women in mind. It is crucial to dismantle gender differences in financial upbringing and their impacts on women's financial futures.Women must take control of their financial futures, especially considering unique challenges like the motherhood penalty and the fact that 74% of women may end up single in retirement. Therefore, young women should carefully explore career choices considering the gender pay gap and the importance of selecting fields with flexibility around child-rearing. In terms of investing, women are found to be more cautious but achieve superior returns. With the looming Great Wealth Transfer women will have greater opportunities to influence investment patterns and philanthropy. Finally, it’s important to be aware of and advocate for policies that fortify retirement programs and promote gender equity.

Draw your own conclusions

|

Learn how to teach with inquiry.

Many of these lesson plans were sponsored in part by the Library of Congress Teaching with Primary Sources Eastern Region Program, coordinated by Waynesburg University, the History and Social Studies Education Faculty at Plymouth State University, and the Patrons of the Remedial Herstory Project. |

|

Lesson Plans from Other Organizations

- The National Women's History Museum has lesson plans on women's history.

- The Guilder Lehrman Institute for American History has lesson plans on women's history.

- The NY Historical Society has articles and classroom activities for teaching women's history.

- Unladylike 2020, in partnership with PBS, has primary sources to explore with students and outstanding videos on women from the Progressive era.

- The Roy Rosenzweig Center for History and New Media has produced recommendations for teaching women's history with primary sources and provided a collection of sources for world history. Check them out!

- The Stanford History Education Group has a number of lesson plans about women in US History.

Period Specific Lesson Plans from Other Organizations

- C3 Teachers: This inquiry leads students through an investigation of the LGBTQ+ movement, primarily driven by the history of the movement through various accounts and perspectives. The compelling question—What makes a movement successful?—does not address whether or not the movement was successful, but instead assesses the components of a movement and whether the movement is in a period of growth or has already peaked. Although the focus of this inquiry is on the LGBTQ+ movement, parallels can be drawn to other social movements in history with respect to organization, activism, and overall execution, including the Civil Rights Movement or the women’s suffrage and rights movements. Specifically, this inquiry looks at four different aspects that can potentially shape a movement in its foundation as well as its rise, namely public reaction, government leaders and policies, Supreme Court cases, and personal experiences. Throughout the inquiry, students will examine each individual aspect independently, evaluating the merits, strengths, and significance of each provided source in the “Movement Analysis Organization Chart,” but the summative task will require a compilation and synthesis of the sources in this investigation in order to form an argument to address the compelling question.

- Voices of Democracy: In the speech Clinton positioned the United States as the moral authority in monitoring and enforcing sanctions for global human trafficking, while at the same time reiterating the importance of international cooperation and partnerships.

- Clio: In 1972, feminists in Washington, D.C. founded the nation’s first rape crisis center. Other centers were soon established across the country. In 1994, Congress passed the Violence Against Women Act (VAWA). The act was created in response to the nation-wide, grassroots work of activists concerned with domestic violence, sexual assault, date rape, and stalking. This lesson introduces students to the history of efforts to stop violence against women.

- National Women’s History Museum: How has the Supreme Court shaped the lives of American women between 1908-2005? Students will analyze one of four Supreme Court cases that relate to the constitutional rights of women decided between 1908-2005. Students will become mini-experts on one Supreme Court cases and they will be exposed to the content, themes, and questions from the other three cases via peer to peer instruction of their classmates. The goal of this lesson is to introduce students to a broad range of Supreme Court cases that have impacted American women and to have them develop a working knowledge and expertise of at least one case by using primary sources such as the case ruling and secondary sources that will help students to understand the context.

- National History Day: Patsy Takemoto Mink (1927-2002) was born in Hawaii. She studied in Pennsylvania and Nebraska before moving back to Hawaii to earn her undergraduate degree and eventually received her J.D. from the University of Chicago in 1951. She moved back to Hawaii with her husband, John Francis Mink, and founded the Oahu Young Democrats in 1954. In the 1950s, Mink served as both a member of the territorial house of representatives and Hawaii Senate. After Hawaii achieved statehood in 1959, Mink unsuccessfully ran for the U.S. House of Representatives. Mink campaigned for the second representative seat in 1964 and won, making her the first woman of color and first Asian American woman to be elected to Congress. Mink is best known for her support of President Lyndon B. Johnson’s Great Society legislation, as well as her advocacy for women’s issues and equal rights. Mink worked tirelessly to earn support for the critical Title IX Amendment from her comprehensive education bill called Women’s Education Equity Act. Mink took a break from Congress after an unsuccessful bid for the Senate, but returned to Congress in 1990 and served until her death in September 2002.

- C3 Teachers: This twelfth grade annotated inquiry leads students through an investigation of a hotly debated issue in the United States: the gender wage gap. The compelling question “What should we do about the gender wage gap?” asks students to grapple not only with how to quantify and interpret the gap but also to consider ways of addressing the problem. Throughout the inquiry, students consider the degree to which economic inequality reflects social, political, or economic injustices or whether it simply reflects individual choices and the role the government should play in decreasing income inequality. Although this inquiry is rooted in a question about economics, no social issue is fully understood without examining a range of economic, historical, geographic, and political concepts in order to craft a full-bodied, evidence-based argument. This inquiry looks at the complexity of the gender wage gap issue through all four social studies disciplines. Students examine the structural factors that influence women’s choices as well as historical (e.g., Equal Pay Act of 1963) and pending (e.g., Paycheck Fairness Act) legislative efforts. Ultimately, students must find a way to measure the gender wage gap, determine if it is an issue worth addressing, and, if so, how to best address it, including private and public sector solutions.

Ellevest

Ellevest is a company that supports women as they make investments. On their site they have articles for women as they consider retirement, divorce, wealth management, and home ownership. Their website states:

"Things are just different for women. Having a financial plan that actually considers those differences is key to building your wealth and reaching your goals... Ellevest was built specifically to account for women’s differences. Traditional financial companies weren't. Women earn 83 cents for every dollar earned by men. That’s a $900k disparity (or more) over a lifetime. 74% of women die single — i.e. we ultimately benefit from staying in control of our own finances. 62% of women say they have unique investment needs that aren’t understood by other advisors."

Women's Personal Finance

This educational tool produces resources for women about personal finance. Their website states:

"Women’s Personal Finance is a community of women and non binary folks who have a common goal of setting and achieving financial goals. We believe all people, no matter their money story or net worth, have valuable things to bring to the table in supporting one another and that community is priceless."

Ellevest is a company that supports women as they make investments. On their site they have articles for women as they consider retirement, divorce, wealth management, and home ownership. Their website states:

"Things are just different for women. Having a financial plan that actually considers those differences is key to building your wealth and reaching your goals... Ellevest was built specifically to account for women’s differences. Traditional financial companies weren't. Women earn 83 cents for every dollar earned by men. That’s a $900k disparity (or more) over a lifetime. 74% of women die single — i.e. we ultimately benefit from staying in control of our own finances. 62% of women say they have unique investment needs that aren’t understood by other advisors."

Women's Personal Finance

This educational tool produces resources for women about personal finance. Their website states:

"Women’s Personal Finance is a community of women and non binary folks who have a common goal of setting and achieving financial goals. We believe all people, no matter their money story or net worth, have valuable things to bring to the table in supporting one another and that community is priceless."

Remedial Herstory Editors. "1. PERSONAL FINANCE." The Remedial Herstory Project. January 1, 2024. www.remedialherstory.com.

|

Consulting TeamKelsie Brook Eckert, Project Director

Coordinator of Social Studies Ed. at Plymouth State University Dr. Linda Upham-Bornstein Teaching Lecturer at Plymouth State University Taylor Maine Intern with the Remedial Herstory Project |

EditorsDr. Barbara Tischler

|

Nonfiction's on Economics

In Fairy Play, Rodsky interviewed more than five hundred men and women from all walks of life to figure out what the invisible work in a family actually entails and how to get it all done efficiently.

|

In The Double X Economy, Scott argues on the strength of hard data and on-the-ground experience that removing those barriers to women’s success is a win for everyone, regardless of gender.

|

In this short, accessible primer, Bell Hooks explores the nature of feminism and its positive promise to eliminate sexism, sexist exploitation, and oppression.

|

In Smart Women Love Money, Finn paves the way forward by showing you that the power of investing is the last frontier of feminism. Finn shares five simple and proven strategies for a woman at any stage of her life, whether starting a career, home raising children, or heading up a major corporation.

|

In Financial Feminist, Dunlap distills the principles of her shame- and judgment-free approach to paying off debt, figuring out your value categories to spend mindfully, saving money without monk-like deprivation, and investing in order to spend your retirement tanning in Tulum.

|

Caroline Criado Perez investigates this shocking root cause of gender inequality in Invisible Women. Examining the home, the workplace, the public square, the doctor’s office, and more, Criado Perez unearths a dangerous pattern in data and its consequences on women’s lives.

|

Written in Hooks's characteristic direct style, Feminist Theory embodies the hope that feminists can find a common language to spread the word and create a mass, global feminist movement.

|

How to teach with Films:

Remember, teachers want the student to be the historian. What do historians do when they watch films?

- Before they watch, ask students to research the director and producers. These are the source of the information. How will their background and experience likely bias this film?

- Also, ask students to consider the context the film was created in. The film may be about history, but it was made recently. What was going on the year the film was made that could bias the film? In particular, how do you think the gains of feminism will impact the portrayal of the female characters?

- As they watch, ask students to research the historical accuracy of the film. What do online sources say about what the film gets right or wrong?

- Afterward, ask students to describe how the female characters were portrayed and what lessons they got from the film.

- Then, ask students to evaluate this film as a learning tool. Was it helpful to better understand this topic? Did the historical inaccuracies make it unhelpful? Make it clear any informed opinion is valid.

|

Fair Play (2022)

Follows three families on their journey to better balance their home life style. They are fighting problems that affect millions of couples and families across the country and even the globe. IMDB |

|

Bibliography

Daly, Lyle. “Investing for Women: What You Should Know: When it comes to investing, women and men differ. Here's what the research says.” Motley Fool. September 26, 2023. https://www.fool.com/research/women-in-investing-research/#:~:text=Women%20are%20more%20conservative%20investors&text=It%20starts%20with%20a%20more,to%20hop%20on%20investing%20trends.

Goldin, Claudia. Career and Family: Women's Century-long Journey Toward Equity (Princeton, New Jersey, Princeton University Press, 2021).

Green, Emily. “The Great Wealth Transfer.” Ellevest. JANUARY 16, 2024. https://www.ellevest.com/magazine/investing/great-wealth-transfer

Krawcheck, Sallie. “18 Truths About Women and Money.” Ellevest. DECEMBER 8, 2020. https://www.ellevest.com/magazine/disrupt-money/truths-about-women-and-money.

Pisarcik, Ian. “Women Outnumber Men in US Law School Classrooms, but Statistics Don’t Tell the Full Story.” Jurist. JANUARY 17, 2024. https://www.jurist.org/commentary/2024/01/women-outnumber-men-in-us-law-school-classrooms-but-statistics-dont-tell-the-full-story/#:~:text=According%20to%20the%20most%20recent,percent%20of%20all%20law%20students.

Reeves, Richard V. Of Boys and Men: Why the Modern Male Is Struggling, Why It Matters, and What to Do About It. Washington, D.C.: Brookings Institution Press, 2022.

Reeves, Richard V. & Isabel V. Sawhill, "Men's Lib." The New York Times. November 14, 2015. https://www.nytimes.com/2015/11/15/opinion/sunday/mens-lib.html?_r=0.

“Women and Retirement: Not-So Golden Years.” American Association of University Women. https://www.aauw.org/issues/equity/retirement/.

Goldin, Claudia. Career and Family: Women's Century-long Journey Toward Equity (Princeton, New Jersey, Princeton University Press, 2021).

Green, Emily. “The Great Wealth Transfer.” Ellevest. JANUARY 16, 2024. https://www.ellevest.com/magazine/investing/great-wealth-transfer

Krawcheck, Sallie. “18 Truths About Women and Money.” Ellevest. DECEMBER 8, 2020. https://www.ellevest.com/magazine/disrupt-money/truths-about-women-and-money.

Pisarcik, Ian. “Women Outnumber Men in US Law School Classrooms, but Statistics Don’t Tell the Full Story.” Jurist. JANUARY 17, 2024. https://www.jurist.org/commentary/2024/01/women-outnumber-men-in-us-law-school-classrooms-but-statistics-dont-tell-the-full-story/#:~:text=According%20to%20the%20most%20recent,percent%20of%20all%20law%20students.

Reeves, Richard V. Of Boys and Men: Why the Modern Male Is Struggling, Why It Matters, and What to Do About It. Washington, D.C.: Brookings Institution Press, 2022.

Reeves, Richard V. & Isabel V. Sawhill, "Men's Lib." The New York Times. November 14, 2015. https://www.nytimes.com/2015/11/15/opinion/sunday/mens-lib.html?_r=0.

“Women and Retirement: Not-So Golden Years.” American Association of University Women. https://www.aauw.org/issues/equity/retirement/.